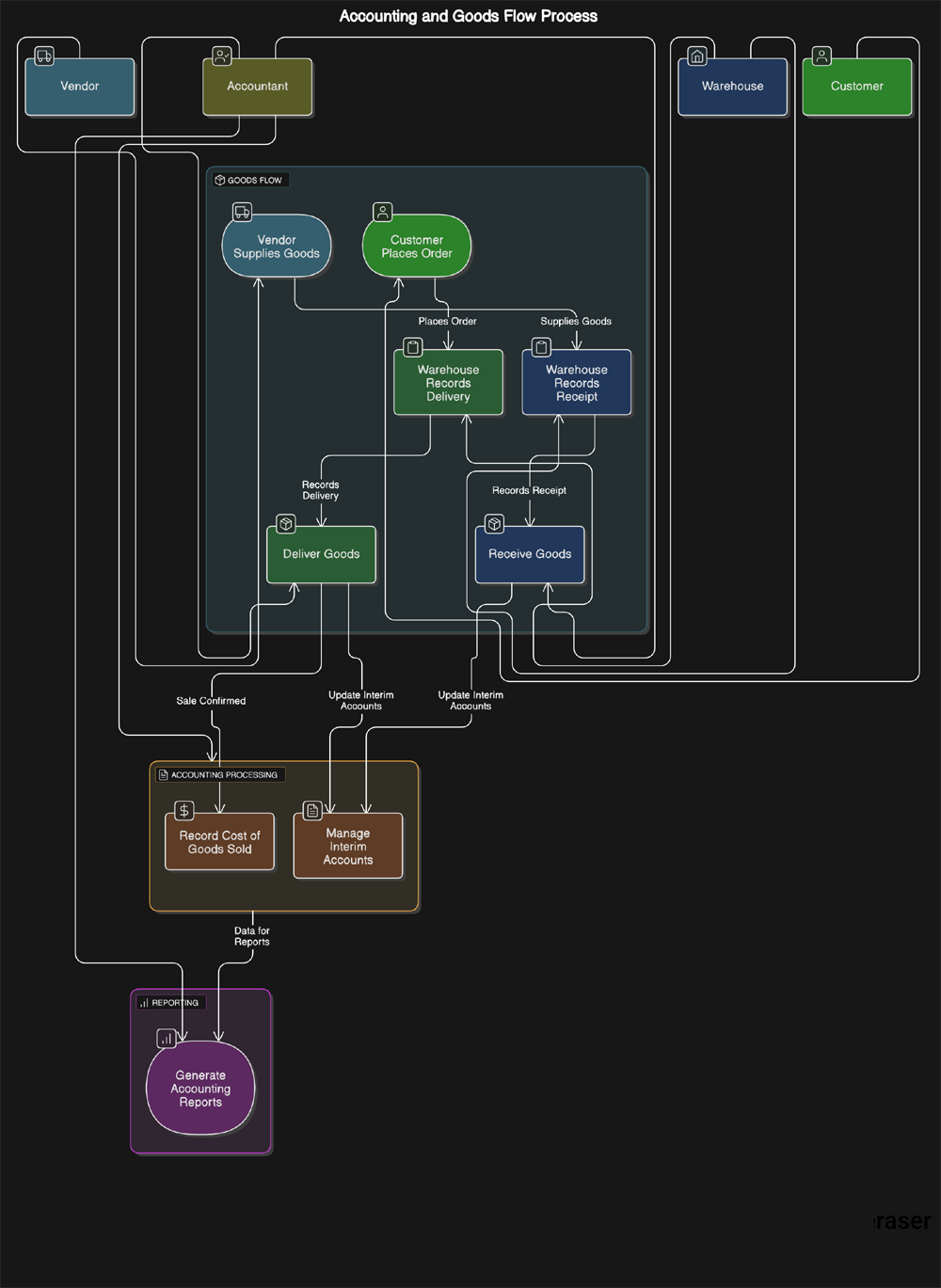

What Are Interim Accounts in Odoo?

Interim accounts in Odoo are temporary holding accounts used during specific accounting processes—especially during stock/inventory valuation in automated inventory accounting. Their primary purpose is to bridge the gap between inventory movements and financial transactions until the final accounting entries can be confirmed.

Purpose of Interim Accounts

- Track Goods in Transit: When goods are delivered or received but not yet invoiced (or vice versa), interim accounts hold the value temporarily.

- Accrual Accounting Compliance: Supports proper revenue/cost recognition before final confirmation (especially in accrual-based accounting).

- Automatic Journal Entries: Odoo uses interim accounts to automatically record entries during stock moves.

Types of Interim Accounts in Odoo

| Account Type | Description |

| Stock Interim (Received) | Used when goods are received but vendor invoice is not yet booked. |

| Stock Interim (Delivered) | Used when goods are delivered but customer invoice is not yet created. |

| Stock Valuation Account | Final account that holds the value of the current stock in inventory. |

Use Case Example

Scenario: A company receives 100 units of raw materials worth $10/unit.

- Goods Receipt (no invoice yet):

Odoo automatically makes this journal entry:

Debit: Stock Interim (Received) : $1,000

Credit: GR/IR (or Inventory Received Not Billed) : $1,000

- Vendor Invoice Created Later:

The entry is reversed and replaced with:

Debit: GR/IR (clears interim) : $1,000

Credit: Accounts Payable : $1,000

1. Accounts Payable (Vendor Purchase Process)

Purpose

To track the value of goods received but not yet invoiced from vendors.

Flow Overview

- Purchase Order is created.

- Goods Receipt is recorded (Stock In).

- Interim accounting uses a Stock Interim (Received) account.

- When Vendor Bill is posted:

- Interim is cleared.

- Accounts Payable is updated.

- Interim is cleared.

Journal Entries

On Goods Receipt:

Debit: Stock Valuation Account (e.g., Raw Materials)

Credit: Stock Interim (Received)

On Vendor Bill:

Debit: Stock Interim (Received)

Credit: Accounts Payable

2. Accounts Receivable (Customer Sales Process)

🎯 Purpose

To track the value of goods delivered but not yet invoiced to customers.

🔄 Flow Overview

- Sales Order is confirmed.

- Goods Delivery is recorded (Stock Out).

- Interim accounting uses a Stock Interim (Delivered) account.

- When Customer Invoice is posted:

- Interim is cleared.

- Revenue and Accounts Receivable are updated.

- Interim is cleared.

Journal Entries

- On Goods Delivery:

Debit: Stock Interim (Delivered)

Credit: Stock Valuation Account (e.g., Finished Goods)

- On Customer Invoice:

Debit: Accounts Receivable

Credit: Stock Interim (Delivered)

Why This Matters

- Ensures real-time and accurate accounting for inventory-related transactions.

- Complies with accrual accounting—matching income and expenses to the correct period.

- Provides a clear audit trail for goods in transit, reducing discrepancies.

Summary of Odoo’s Benefits Over Others

| Benefit | Why Odoo Stands Out |

| Transparency | Easy to trace interim entries linked to stock operations |

| Customization | Fully customizable interim logic per product or warehouse |

| Audit Trail Simplicity | Stock moves, invoices, and journals are tightly integrated |

Example Use Case Advantage

In Odoo:

- You can have different interim accounts per warehouse, per product category.

- A manufacturing company can handle partial receipts and still maintain financial accuracy automatically—without manual adjustments.

In NetSuite / Navision:

- Requires scripting or customizing posting groups for the same granularity.

- Tends to be more rigid out-of-the-box.

Below is a step-by-step explanation of inventory movement and its accounting effects in Odoo, separated into payable (receiving goods from a vendor) and receivable (selling goods to a customer) scenarios. Let’s use real-time values to make the process clear and assume a simple setup with specific costs and prices.

Scenario Setup

- Product: Widget A

- Cost Price: $100 per unit (cost to purchase or produce)

- Sale Price: $150 per unit

- Initial Inventory: 0 units

- Accounts Involved:

- Inventory (Asset)

- Stock Interim (Received) (Asset) – Temporary account for goods received

- Stock Interim (Delivered) (Asset) – Temporary account for goods delivered

- Accounts Payable (Liability)

- Accounts Receivable (Asset)

- COGS (Cost of Goods Sold, Expense)

- Sales Revenue (Income)

- Bank (Asset)

Let’s walk through each scenario separately.

Payable Scenario: Receiving Goods from a Vendor

In this scenario, we purchase 10 units of Widget A from a vendor at $100 each (total $1,000), with payment terms on credit (we pay later).

Step 1: Purchase Order Creation

- Action: We create a purchase order for 10 units.

- Accounting Effect: None. This is just a commitment to buy, so no journal entries are recorded yet.

Step 2: Receiving Goods

- Action: The 10 units are delivered to our warehouse.

- Accounting Effect: Odoo records the receipt of goods in a temporary account before moving them to inventory.

- Journal Entry:

- Dr Inventory : $1,000

- Cr Stock Interim (Received): $1,000

- Explanation: The Inventory account isn’t updated yet. The Stock Interim (Received) account holds the value of goods received until fully processed, and Accounts Payable reflects our liability to the vendor.

Step 3: Vendor Bill Recording

- Action: The vendor sends a bill, which we record in Odoo.

- Accounting Effect: In many Odoo setups, receiving goods and recording the bill are linked. If separate, the bill confirms the liability, but the key entry is already made in Step 2.

- Journal Entry: No new entry if Step 2 already recorded the liability. Otherwise:

- Dr Stock Interim (Received): $1,000

- Cr Accounts Payable: $1,000

- Explanation: For simplicity, assume Step 2 covered this. The bill just validates the transaction.

Step 4: Reconciling Interim Accounts

- Action: After processing (e.g., quality checks), the goods are officially moved to inventory.

- Accounting Effect: The value transfers from the interim account to the Inventory account.

- Journal Entry:

- Debit Inventory: $1,000

- Credit Stock Interim (Received): $1,000

- Explanation: Now, Inventory reflects the actual stock value ($1,000), and Stock Interim (Received) is cleared to $0.

Step 5: Payment to Vendor

- Action: We pay the vendor the full amount owed.

- Accounting Effect: The liability is settled using cash from the bank.

- Journal Entry:

- Debit Accounts Payable: $1,000

- Credit Bank: $1,000

- Explanation: Accounts Payable is cleared, and the Bank account decreases by $1,000.

Final Account Balances (Payable Scenario Only)

- Inventory: $1,000 (10 units × $100)

- Stock Interim (Received): $0

- Accounts Payable: $0

- Bank: -$1,000 (assuming we started with $0 and paid $1,000)

This concludes the payable scenario. Now, let’s move to the receivable scenario.

Receivable Scenario: Selling Goods to a Customer

In this scenario, we sell 5 units of Widget A to a customer at $150 each (total $750), with payment terms on credit (they pay later). Assume the 10 units from the payable scenario are in stock.

Step 1: Sales Order Creation

- Action: We create a sales order for 5 units.

- Accounting Effect: None. This is just a commitment to sell, so no journal entries are recorded yet.

Step 2: Delivering Goods

- Action: We deliver 5 units to the customer from our inventory.

- Accounting Effect: The cost value of the goods leaves Inventory and moves to a temporary account.

- Journal Entry:

- Debit Stock Interim (Delivered): $500 (5 units × $100 cost price)

- Credit Inventory: $500

- Explanation: Inventory decreases by $500 (reflecting 5 units removed), and Stock Interim (Delivered) temporarily holds the cost of goods delivered but not yet invoiced.

Step 3: Recording COGS

- Action: Since the goods are sold, we record the cost of goods sold (COGS).

- Accounting Effect: COGS is updated to reflect the expense of the sale.

- Journal Entry:

- Debit COGS: $500 (5 units × $100)

- Credit Stock Interim (Delivered): $500

- Explanation: COGS records the $500 cost of the sold goods, and Stock Interim (Delivered) is cleared to $0.

Step 4: Customer Invoice Creation

- Action: We issue an invoice to the customer for the sale price.

- Accounting Effect: Revenue is recognized, and we record what the customer owes us.

- Journal Entry:

- Debit Accounts Receivable: $750 (5 units × $150)

- Credit Sales Revenue: $750

- Explanation: Accounts Receivable increases by $750 (the amount the customer owes), and Sales Revenue reflects the income from the sale.

Step 5: Receiving Payment from Customer

- Action: The customer pays us the full amount.

- Accounting Effect: The receivable is settled, and cash is received.

- Journal Entry:

- Debit Bank: $750

- Credit Accounts Receivable: $750

- Explanation: Accounts Receivable is cleared, and the Bank account increases by $750.

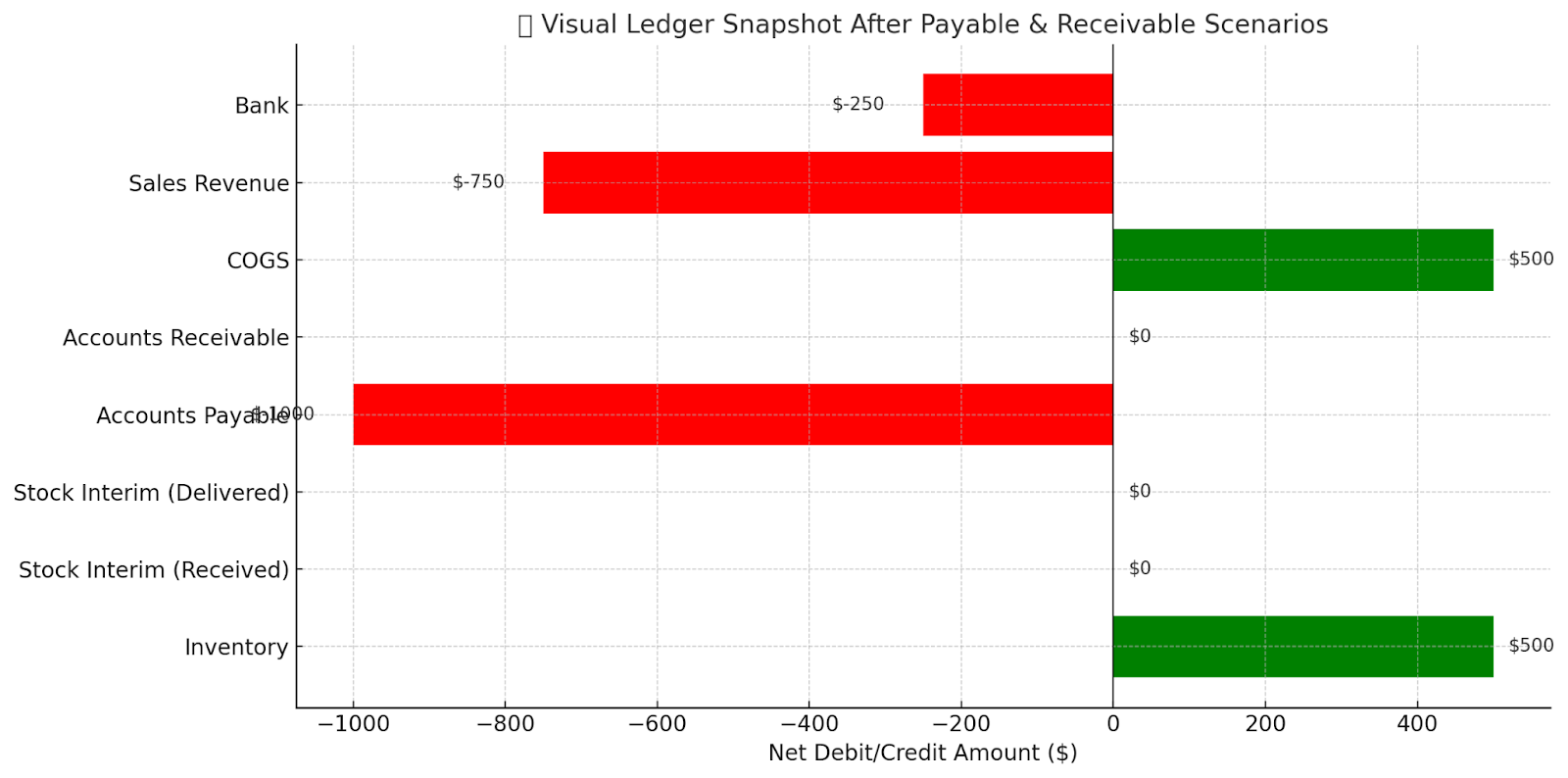

Final Account Balances (After Both Scenarios)

Assuming we combine the payable and receivable scenarios:

- Inventory: $500 (10 units received – 5 units sold = 5 units × $100)

- Stock Interim (Received): $0

- Stock Interim (Delivered): $0

- Accounts Payable: $0 (paid in full)

- Accounts Receivable: $0 (paid in full)

- COGS: $500 (cost of 5 units sold)

- Sales Revenue: $750 (revenue from 5 units sold)

- Bank: -$250 (paid $1,000 to vendor, received $750 from customer)

- Bank: -$250 (paid $1,000 to vendor, received $750 from customer)

Key Takeaways

- Payable Scenario: Tracks goods received from a vendor, using Stock Interim (Received) to bridge the gap between receipt and inventory recognition, ending with payment to the vendor.

- Receivable Scenario: Tracks goods sold to a customer, using Stock Interim (Delivered) to manage the cost of goods until COGS is recorded, ending with payment from the customer.

- Interim Accounts: These temporary accounts (Stock Interim Received and Delivered) ensure accurate timing between physical inventory movements and financial records.

- Profit: The difference between Sales Revenue ($750) and COGS ($500) is $250, which would appear in the income statement, not directly in the Bank account.

Difficulty of Maintaining Three-Way Matching Without Interim Accounts in Accounting

Three-way matching is an accounting process that verifies the accuracy and legitimacy of vendor payments by comparing three key documents: the purchase order (PO), the receiving report (or goods receipt), and the vendor’s invoice. Interim accounts, such as “Goods Received Not Invoiced” or accrued liability accounts, are often used to temporarily record transactions during this process until all documents are matched. Without interim accounts, maintaining three-way matching becomes significantly more challenging. Below, I’ll explain why, breaking it down into key aspects of the process.

1. Timing Discrepancies Between Physical and Financial Transactions

Interim accounts bridge the gap between when goods are physically received and when the invoice arrives. Without them:

- Option A: Delay Recording Until Invoice Arrives

- If no entry is made until the invoice is received, the inventory and associated liabilities remain unrecorded until all three documents are available. For example, if goods worth $1,000 are received on December 31 but the invoice arrives on January 5, the financial statements for December would understate both inventory (an asset) and liabilities. This delay distorts real-time financial reporting and complicates inventory management.

- Option B: Record Directly to Accounts Payable Based on PO

- Alternatively, you could record the liability in Accounts Payable based on the PO price when goods are received. However, if the invoice later shows a different amount (e.g., due to price changes or errors), adjustments would be needed, disrupting the matching process and increasing the risk of errors.

- Difficulty: Without interim accounts, you lose the ability to accurately reflect the timing of goods receipt versus invoice processing, making it harder to align the PO, receipt, and invoice seamlessly.

2. Tracking Uninvoiced Receipts

Interim accounts provide a clear way to track goods that have been received but not yet invoiced, which is critical for three-way matching:

- With Interim Accounts: An account like “Goods Received Not Invoiced” shows the value of goods awaiting invoices, simplifying the identification of pending matches.

- Without Interim Accounts: You’d need to rely on manual tracking, subsidiary ledgers, or additional documentation to monitor which receipts still need invoices. This increases the risk of overlooking transactions or duplicating efforts during matching.

- Difficulty: The lack of a dedicated account makes it labor-intensive and error-prone to determine which goods have been received but not invoiced, complicating the verification process.

3. Accuracy in Financial Reporting

Accurate financial statements depend on timely recognition of assets and liabilities:

- With Interim Accounts: When goods are received, inventory is debited, and an interim account (e.g., “Goods Received Not Invoiced”) is credited. Once the invoice is matched, the interim account is cleared, and Accounts Payable is updated. This ensures financials are correct at every stage.

- Without Interim Accounts:

- Delaying entries until the invoice arrives understates assets and liabilities in the interim period.

- Recording directly to Accounts Payable risks inaccuracies if the invoice differs from the PO, requiring subsequent corrections.

- Difficulty: Inaccurate or delayed financial data undermines the reliability of the records used for three-way matching, making it harder to trust the quantities and amounts being compared.

4. Control and Auditability

Interim accounts enhance internal controls and provide a clear audit trail:

- With Interim Accounts: The separation of goods receipt (recorded in an interim account) and invoice processing (finalized in Accounts Payable) allows different personnel to handle each step, reducing the risk of fraud or errors. The interim account serves as a checkpoint for matching.

- Without Interim Accounts: The process may require simultaneous handling of receipts and invoices, weakening segregation of duties. It also obscures the audit trail, as there’s no distinct record of goods received but not invoiced.

- Difficulty: Weaker controls increase the risk of mismatches, overpayments, or fraudulent payments, as the three-way matching process lacks a structured intermediate step.

5. Efficiency in Automated Systems

Modern accounting systems rely on interim accounts to streamline three-way matching:

- With Interim Accounts: In software like Odoo, interim accounts (e.g., “Stock Interim”) automate the tracking of uninvoiced receipts and generate reports on unmatched transactions, improving efficiency.

- Without Interim Accounts: Manual intervention becomes necessary to reconcile receipts and invoices, slowing down the process and increasing the likelihood of mistakes, especially in high-volume environments.

- Difficulty: The absence of automation support makes three-way matching more time-consuming and less scalable, particularly for businesses with frequent transactions.

Example Scenario

Consider a company receiving 100 units of a product worth $1,000 on December 31, with the invoice arriving on January 5:

- With Interim Accounts:

- Dec 31: Debit Inventory $1,000, Credit Goods Received Not Invoiced $1,000.

- Jan 5: Debit Goods Received Not Invoiced $1,000, Credit Accounts Payable $1,000 (after matching PO, receipt, and invoice).

- Result: Accurate financials on Dec 31 and a smooth matching process.

- Without Interim Accounts:

- Option 1: Delay Recording: No entry on Dec 31. On Jan 5, Debit Inventory $1,000, Credit Accounts Payable $1,000. December financials are incomplete.

- Option 2: Record to Accounts Payable: On Dec 31, Debit Inventory $1,000, Credit Accounts Payable $1,000. If the invoice on Jan 5 shows $1,050, adjustments are needed, complicating the match.

- Result: Either delayed reporting or error-prone adjustments, both hindering three-way matching.

Conclusion

Maintaining three-way matching without interim accounts is significantly more difficult because:

- Timing discrepancies lead to delayed or inaccurate recordings.

- Tracking uninvoiced receipts becomes manual and error-prone.

- Financial reporting loses accuracy and timeliness.

- Internal controls and auditability are weakened.

- Efficiency drops, especially in automated systems.

Interim accounts provide a structured, controlled, and efficient way to manage the matching of purchase orders, receiving reports, and invoices. Without them, the process becomes more cumbersome, less reliable, and more susceptible to errors, making it a critical challenge for effective accounting.

Key Benefits Highlighted

The image also incorporates small icons or text bubbles around the flowchart to emphasize specific advantages:

- Accurate Reporting

- Interim accounts ensure transactions are recorded correctly at each stage, providing real-time financial clarity even before final invoicing.

- Efficient Reconciliation

- By temporarily holding transactions, interim accounts simplify matching goods received with invoices, reducing errors and saving time.

- Better Inventory Control

- They allow businesses to track goods as soon as they arrive, improving inventory accuracy and management.

Why This Matters for Your Business

Without interim accounts, accounting can feel like untangling a knot—stressful and prone to mistakes. With them, Odoo transforms the process into a clear, manageable workflow. This visual contrast—chaos versus order—makes it easy to see why interim accounts are a game-changer for businesses using Odoo.

In summary, Odoo’s interim accounts bring accuracy, efficiency, and control to your financial and inventory processes. This makes them an essential tool for any business looking to simplify operations and enhance reporting—all depicted clearly in a single, impactful image.